SMM's Latest Market Update (July 30): Mainstream transaction prices for Pr-Nd oxide: 531,500 yuan/mt (up 11,000 yuan from the previous day), mainstream transaction prices for Pr-Nd alloy: 645,000 yuan/mt (up 20,000 yuan from the previous day). In addition to Pr-Nd oxide and alloy, single Pr oxide, single Nd oxide, Pr metal, and Nd metal all showed significant increases exceeding 10,000 yuan/mt.

In our previous discussions, we analyzed the core driving forces behind this round of price increases—improved fundamentals coupled with rising market sentiment. Today, we shift our focus to the end of the industry chain, concentrating on the end-users who "foot the bill": How have they reacted to this sharp price surge? What pressures are they facing? It should be noted that end-use applications are diverse. This article is based on observations of core samples, and any omissions are welcome for correction and discussion. To understand the end-users, we inevitably need to delve into the two core transmission links: magnetic materials and motors. Let's break them down one by one.

Magnetic Material Factory: Pressures and Strategies Coexist

Market Review

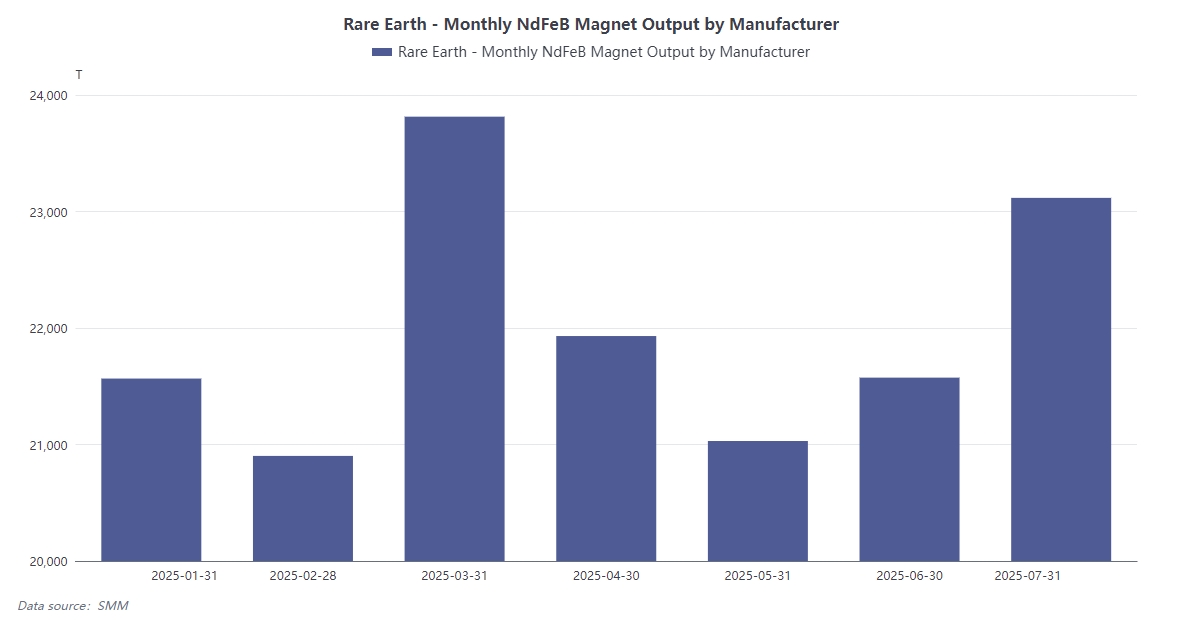

The year 2025 was like a "roller coaster" ride for the magnetic material industry: production at the beginning of the year was hindered by holidays → demand recovered rapidly in February-March → impacted by export control measures in April → hit a low in May → gradually recovered in June as Sino-US relations improved.

Throughout this tumultuous year, magnetic material factories struggled to navigate the market's waves. At the beginning of the year, holidays limited the operating rate, preventing enterprises from fully utilizing their capacity, resulting in slow revenue growth. The rapid rebound in demand in February-March brought hope to magnetic material factories, with a significant increase in orders and production lines operating at full capacity.

However, the sudden export control measures in April dealt a heavy blow to enterprises' production schedules, leading to a sharp decline in overseas orders and severe inventory backlogs. May saw an even deeper trough, with enterprises facing immense operational pressures, and some small and medium-sized magnetic material factories even experiencing tight capital chains. It was not until June, with the easing of Sino-US relations, that the market gradually recovered, and magnetic material factories began to slowly revive.

Current Responses

In the face of soaring raw material costs, magnetic material producers have adopted differentiated strategies, but the main theme is clear.

Some enterprises intend to leverage the price hikes to boost short-term orders. They believe that the rise in raw material prices is a common phenomenon in the industry under the current market conditions. By moderately increasing product prices, they can alleviate cost pressure to a certain extent while also testing the market's acceptance of price increases.

If the market's response to the price hikes is moderate, they can increase short-term earnings and accumulate funds for subsequent development. However, long-term contract customers who have locked in low-priced raw materials face a difficult choice—executing the contracts will lead to marginal losses, while breaching them will damage their reputation. For these customers, magnetic material producers are in a dilemma. If they continue to supply at long-term contract prices, with the continuous rise in raw material costs, the enterprises will face increasing losses. However, if they choose to breach the contracts, they will not only lose customer trust but may also face legal disputes and damage to their market reputation.

The industry's overall consensus is "mild transmission and dynamic negotiation": choosing a "small steps" approach to price increases, negotiating cost-sharing with downstream customers in batches, and striving to reduce losses (important customers can bear slight losses). This strategy aims to avoid customer loss due to significant price hikes and jointly address the pressure of rising costs through communication and negotiation with downstream customers. For important customers, magnetic material producers are willing to sacrifice short-term profits to a certain extent to maintain long-term stable cooperative relationships.

In terms of market structure, top-tier enterprises rely on capacity, technological, and financial barriers to continuously absorb incremental overseas orders, compressing the market share space of mid-to-low-tier producers. Top-tier enterprises can obtain more favorable prices in raw material procurement due to their scale advantages, reducing costs. Advanced technology makes their product quality more competitive, meeting the needs of high-end customers. Adequate funds ensure enterprises' investments in R&D, production equipment updates, etc., further enhancing their strength. In contrast, mid-to-low-tier producers, due to limited capacity, cannot undertake large-scale orders and lack bargaining power in raw material procurement, resulting in high costs. Their relatively backward technological levels make their products less competitive in the market, leading to a continuous erosion of their market share by top-tier enterprises. This reflects that after upstream concentration guided by policies, the magnetic material industry has entered a deep integration stage dominated by market competition. With the advancement of industry integration, market resources will further concentrate on top-tier enterprises, and mid-to-low-tier enterprises face severe challenges of transformation, upgrading, or being eliminated.

Motor Factory: High Tolerance for Costs, but Bounded Acceptance of Prices

Impact of Cost Structure

The proportion of permanent magnets in the total cost of permanent magnet motors is generally not high (commonly believed to be below 10%), which has led to feedback from leading motor factories that "current production plans have not yet been disrupted." However, this does not mean they are indifferent to prices.

Although the cost proportion of permanent magnets is relatively low, in the case of large-scale production, even minor fluctuations in their costs can impact the overall profitability of enterprises. Moreover, the profit margins of motor factories are inherently limited, necessitating cautious handling of any cost increases. Due to the long-term downward trend of Pr-Nd raw material prices after reaching a historical high in 2011 (especially stabilizing at low levels from 2022-2024), motor factories generally lack the motivation for "price-locking" procurement (which itself carries significant risks). During the past period of low prices, motor factories became accustomed to a relatively stable raw material price environment and did not develop a consciousness of price-locking procurement. Furthermore, price-locking procurement requires accurate judgments on market price trends, and misjudgments could lead to substantial increases in procurement costs for enterprises.

Determination of Procurement Strategy

The accelerated iteration of car models in the NEV field has led to frequent adjustments in motor technical solutions and even permanent magnet formulations. This characteristic has reinforced the mainstream model of motor factories, which is to "procure based on orders and control inventory risks."

Typically, they replenish stock at market prices only when magnetic material inventory is depleted. The rapid iteration of car models makes it difficult for motor factories to predict future market demand. To avoid the capital occupation and depreciation risks associated with inventory buildup, procuring based on orders has become a safer choice. Only when magnetic material inventory is about to run out do they replenish stock according to market prices to ensure production continuity. Although this procurement model can effectively control inventory risks, it also makes motor factories more passive in the face of raw material price fluctuations.

Key Price Thresholds

In the past, there was a general consensus in the industry that a price range of 530,000-550,000 yuan/mt for Pr-Nd alloy was likely to facilitate transactions, with price-sensitive customers setting their bottom line at around 500,000 yuan/mt. Within this price range, motor manufacturers considered procurement costs to be relatively reasonable, allowing them to maintain a certain profit margin while ensuring product quality.

Realistic Challenges

Currently, the market quote for Pr-Nd alloy has surged to over 650,000 yuan/mt (although there have been sporadic transactions at around 545,000 yuan/mt). For motor manufacturers and end-users at the furthest downstream, the magnitude and pace of the increase far exceeded expectations, leading to widespread resistance.

According to our understanding, the "hesitation threshold" for end-users is around 610,000 yuan/mt. Prices exceeding 600,000 yuan/mt require careful evaluation of procurement necessity, and when prices reach 610,000-620,000 yuan/mt, they tend to adopt a wait-and-see attitude unless it is an urgent order. This clearly reveals the lag in end-user price feedback. Motor manufacturers and end-users find it difficult to bear such high prices. The rapid price increase has exceeded their cost budgets, making them cautious in procurement decisions. End-users begin to hesitate about procurement when prices reach around 610,000 yuan/mt, and need to carefully evaluate the necessity of procurement when prices exceed 600,000 yuan/mt.

When prices reach 610,000-620,000 yuan/mt, they are more inclined to wait and see, except for urgent orders, hoping for a price pullback. This lag in price feedback also brings uncertainty to the market, resulting in a situation where upstream and downstream rare earth players are engaged in mutual game-playing.